Gold investment line of credit

Open a Gold Investment Line of Credit and build your gold position with twice the buying power.

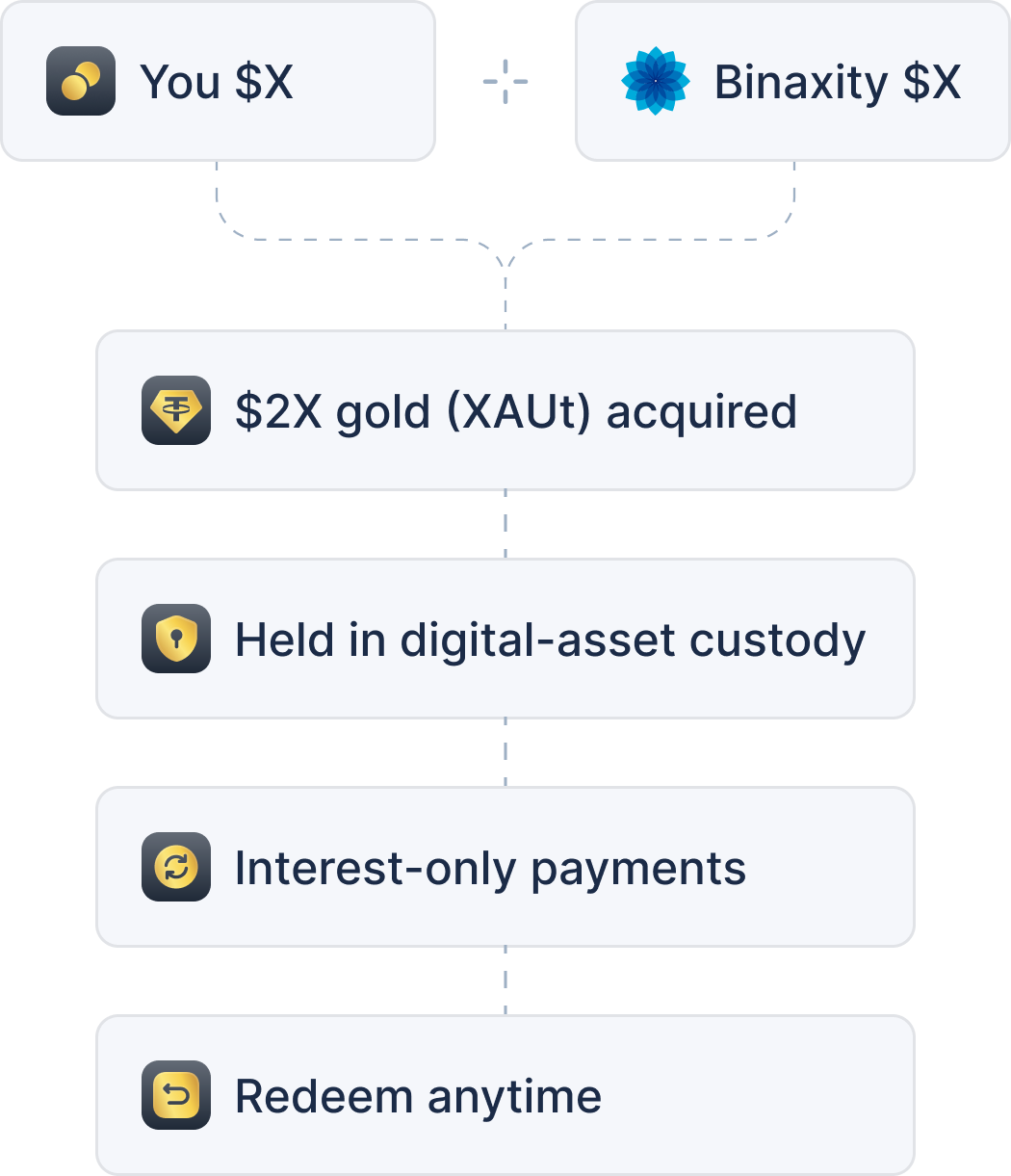

A Gold I-LOC that matches every dollar you contribute 1:1, so you accumulate more gold exposure over time - interest-only payments, no volatility-driven margin calls, and the freedom to redeem your position anytime.

- Bring cash, no gold required

- No volatility-driven margin calls

- Redeem your position anytime

'%3e%3crect%20width='32'%20height='32'%20rx='8'%20fill='url(%23paint2_linear_0_1)'/%3e%3cg%20id='vuesax/bold/shield-tick_2'%3e%3cpath%20id='Vector'%20d='M16.002%206.26257C16.3483%206.26258%2016.6763%206.31133%2016.9072%206.39636L22.4033%208.45496V8.45593C22.8436%208.62368%2023.2644%208.97717%2023.5752%209.42859C23.886%209.88021%2024.0657%2010.3993%2024.0615%2010.8719V18.9755C24.0614%2019.3065%2023.9506%2019.716%2023.7549%2020.1073C23.5594%2020.4982%2023.2984%2020.834%2023.0322%2021.035L17.5322%2025.1444L17.5312%2025.1454C17.1226%2025.4529%2016.566%2025.618%2015.9922%2025.618C15.4182%2025.618%2014.8609%2025.453%2014.4521%2025.1454L14.4512%2025.1444L8.95117%2021.035L8.94922%2021.0331C8.68551%2020.8382%208.42432%2020.504%208.22852%2020.1112C8.03292%2019.7188%207.92196%2019.3067%207.92188%2018.9755V10.8749C7.92193%2010.401%208.10482%209.88127%208.41797%209.42957C8.73104%208.97815%209.15348%208.62301%209.59863%208.45496L15.0957%206.39636L15.0967%206.39734C15.3276%206.31226%2015.6555%206.26257%2016.002%206.26257ZM19.752%2012.37C19.3156%2011.9336%2018.5986%2011.9337%2018.1621%2012.37L14.6562%2015.8739L13.8418%2015.0594C13.4054%2014.6235%2012.6883%2014.6235%2012.252%2015.0594C11.8163%2015.4951%2011.8159%2016.2107%2012.25%2016.6473V16.6483L13.8496%2018.2684L13.8516%2018.2704C14.0755%2018.4943%2014.3625%2018.6004%2014.6465%2018.6005C14.9306%2018.6005%2015.2184%2018.4944%2015.4424%2018.2704L19.7412%2013.9696C20.1885%2013.5324%2020.1877%2012.8057%2019.752%2012.37Z'%20fill='url(%23paint3_linear_0_1)'%20stroke='url(%23paint4_linear_0_1)'%20stroke-width='0.75'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_0_1'%20x1='789'%20y1='-107.089'%20x2='672.373'%20y2='1330.87'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='white'/%3e%3cstop%20offset='1'%20stop-color='%2395CCF3'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_0_1'%20x1='7.47699'%20y1='60'%20x2='105.099'%20y2='146.392'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='white'/%3e%3cstop%20offset='1'%20stop-color='white'%20stop-opacity='0.48'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_0_1'%20x1='16'%20y1='32'%20x2='16'%20y2='0'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231F2937'/%3e%3cstop%20offset='1'%20stop-color='%231F2937'%20stop-opacity='0.68'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint3_linear_0_1'%20x1='8.87256'%20y1='21.985'%20x2='25.559'%20y2='9.92443'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23D4A041'/%3e%3cstop%20offset='0.410355'%20stop-color='%23FBE67B'/%3e%3cstop%20offset='0.635836'%20stop-color='%23F7D14E'/%3e%3cstop%20offset='1'%20stop-color='%23D4A041'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint4_linear_0_1'%20x1='15.9919'%20y1='5.35849'%20x2='15.9919'%20y2='26.5217'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='white'%20stop-opacity='0.2'/%3e%3cstop%20offset='1'%20stop-color='white'%20stop-opacity='0.01'/%3e%3c/linearGradient%3e%3cclipPath%20id='clip0_0_1'%3e%3crect%20width='32'%20height='32'%20rx='8'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'/%3e%3cg%20id='vuesax/bold/refresh-circle_2'%3e%3cg%20id='refresh-circle'%3e%3cpath%20id='Vector'%20d='M11.8125%206.34961H20.1973C21.9486%206.34965%2023.3045%206.87021%2024.2207%207.78711C25.1368%208.70387%2025.6551%2010.0587%2025.6504%2011.8086V20.1904C25.6503%2021.9406%2025.1294%2023.2959%2024.2119%2024.2129C23.2944%2025.1298%2021.9385%2025.6503%2020.1875%2025.6504H11.8125C10.0613%2025.6503%208.70555%2025.1291%207.78809%2024.2109C6.87074%2023.2927%206.34961%2021.9351%206.34961%2020.1797V11.8096C6.34969%2010.0594%206.87061%208.70413%207.78809%207.78711C8.70559%206.87016%2010.0614%206.34969%2011.8125%206.34961ZM13.3506%2010.8428C12.9238%2010.4162%2012.2227%2010.4162%2011.7959%2010.8428L10.2246%2012.4121C9.79818%2012.8383%209.79817%2013.539%2010.2236%2013.9658V13.9668L11.7949%2015.5469L11.7959%2015.5479C12.015%2015.7667%2012.2955%2015.8701%2012.5732%2015.8701C12.851%2015.8701%2013.1315%2015.7667%2013.3506%2015.5479C13.687%2015.2116%2013.7629%2014.7255%2013.5869%2014.3203H17.9258C19.0232%2014.3203%2019.9071%2015.2034%2019.9072%2016.2998C19.9072%2017.3954%2019.0143%2018.2803%2017.9258%2018.2803H13.0039C12.4006%2018.2803%2011.9034%2018.7765%2011.9033%2019.3799C11.9033%2019.9833%2012.4006%2020.4805%2013.0039%2020.4805H17.9258C20.2288%2020.4805%2022.1074%2018.6142%2022.1074%2016.3096C22.1072%2014.0063%2020.2298%2012.1299%2017.9258%2012.1299H13.5469C13.7623%2011.7154%2013.6969%2011.1889%2013.3506%2010.8428Z'%20fill='url(%23paint3_linear_0_1)'%20stroke='url(%23paint4_linear_0_1)'%20stroke-width='0.7'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='bgblur_0_0_1_clip_path'%20transform='translate(72%2068)'%3e%3c/clipPath%3e%3clinearGradient%20id='paint0_linear_0_1'%20x1='789'%20y1='-107.089'%20x2='672.373'%20y2='1330.87'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='white'/%3e%3cstop%20offset='1'%20stop-color='%2395CCF3'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_0_1'%20x1='6.74478'%20y1='60'%20x2='103.843'%20y2='142.698'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='white'/%3e%3cstop%20offset='1'%20stop-color='white'%20stop-opacity='0.48'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_0_1'%20x1='16'%20y1='32'%20x2='16'%20y2='0'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231F2937'/%3e%3cstop%20offset='1'%20stop-color='%231F2937'%20stop-opacity='0.68'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint3_linear_0_1'%20x1='6'%20y1='26'%20x2='27.2516'%20y2='18.6309'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23D4A041'/%3e%3cstop%20offset='0.410355'%20stop-color='%23FBE67B'/%3e%3cstop%20offset='0.769917'%20stop-color='%23F7D14E'/%3e%3cstop%20offset='1'%20stop-color='%23D4A041'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint4_linear_0_1'%20x1='16'%20y1='5.47368'%20x2='16'%20y2='26.5263'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='white'%20stop-opacity='0.2'/%3e%3cstop%20offset='1'%20stop-color='white'%20stop-opacity='0.01'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

What is a Gold Investment Line of Credit?

A Gold I-LOC is built for one purpose: accumulating gold exposure over time. That makes it the opposite of a traditional "gold loan" - where you pledge bullion you already own to borrow cash, and the lender can sell it if the price drops. Useful for liquidity. Not useful if your goal is to own more gold.

This product runs the other way. You're not borrowing against gold - you're building a position. Binaxity doubles your investment, and the combined amount acquires tokenized gold (XAUt) held in digital-asset custody. Bring $1,000, build $2,000 of exposure. You owe interest only on the borrowed half - never principal, never a forced repayment date. Nothing of yours is pledged, and your position isn't liquidated over a rough week.

How a Gold I-LOC differs from a traditional gold loan

On paper, both involve gold and credit. In practice they're built for opposite people. A traditional gold loan serves someone who already owns metal and needs liquidity. A Gold Investment Line of Credit serves someone who wants to build a gold position in the first place - and is structured to avoid the forced-exit mechanics that define collateralized lending.

The difference that matters most is what happens when the price falls. A collateralized gold loan tracks your loan-to-value ratio, and once the price drops far enough you either top up or the lender sells your bullion. A Gold I-LOC has no LTV threshold and no volatility-driven margin call - a falling price lowers the value of your position, but the structure doesn't change and nothing is force-sold. You decide when to exit, not the market.

Collateral

If the price falls

LTV thresholds

Payments

Term & exit

How co-investment works - four steps

Each step is simple on your side and structured on ours. Here's the full path from application to an active gold position.

- 01

Apply and get your credit limit

Complete KYC verification and receive a personalized credit limit. There's no credit-history check - approval is based on your co-investment capacity, not your borrowing past. Approval is typically fast, with manual review in some cases.

- 02

Draw funds and co-invest on your schedule

Contribute in stablecoins when it suits you, pause when it doesn't. Each contribution is matched 1:1 - put in $500, Binaxity lends $500, and $1,000 of gold exposure is acquired for your position. You control the pace.

- 03

Gold is acquired and secured

The combined funds acquire tokenized gold (XAUt) - usually within minutes, up to around 12 hours after funding is confirmed, depending on liquidity and settlement. The XAUt is held in Binaxity's digital-asset custody; the physical gold backing it sits with the XAUt issuer's custodian structure. Your dashboard shows your contribution, the matched loan, the gold acquired (in USD and troy ounces / XAUt units), and your current position value.

- 04

Pay simple monthly interest, build long-term

Your only obligation while the position is open is interest on the borrowed portion. No amortization, no balloon payment, no schedule pushing you to unwind before you're ready. (Interest is variable - see "How your rate works" below.)

What a gold position looks like in practice

Here's a hypothetical walk-through with round numbers. Illustrative only - gold's market price changes continuously, and these are not live quotes.

Position overview

Interest cost

'%3e%3cpath%20id='Vector'%20d='M10.0013%2018.3332C14.6037%2018.3332%2018.3346%2014.6022%2018.3346%209.99984C18.3346%205.39746%2014.6037%201.6665%2010.0013%201.6665C5.39893%201.6665%201.66797%205.39746%201.66797%209.99984C1.66797%2014.6022%205.39893%2018.3332%2010.0013%2018.3332Z'%20stroke='url(%23paint0_linear_0_1)'%20stroke-width='1.66667'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20id='Vector_2'%20d='M10%206.6665V9.99984'%20stroke='url(%23paint1_linear_0_1)'%20stroke-width='1.66667'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20id='Vector_3'%20d='M10%2013.3335H10.0083'%20stroke='url(%23paint2_linear_0_1)'%20stroke-width='1.66667'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='bgblur_0_0_1_clip_path'%20transform='translate(44%20342)'%3e%3c/clipPath%3e%3clinearGradient%20id='paint0_linear_0_1'%20x1='8.39647'%20y1='4.39639'%20x2='8.39647'%20y2='16.609'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231B2B47'/%3e%3cstop%20offset='1'%20stop-color='%232D4877'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_0_1'%20x1='10.4037'%20y1='7.21248'%20x2='10.4037'%20y2='9.65501'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231B2B47'/%3e%3cstop%20offset='1'%20stop-color='%232D4877'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_0_1'%20x1='10.0034'%20y1='13.4973'%20x2='10.0034'%20y2='14.23'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231B2B47'/%3e%3cstop%20offset='1'%20stop-color='%232D4877'/%3e%3c/linearGradient%3e%3cclipPath%20id='clip1_0_1'%3e%3crect%20width='20'%20height='20'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e) Risk note

Risk noteRate is variable and may increase if gold price falls below your reference level (see "How your rate works").

Two scenarios over 12 months

Illustrative example only'%20stroke-width='1.5'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20id='Vector_2'%20d='M5%2012L12%205L19%2012'%20stroke='url(%23paint1_linear_0_1)'%20stroke-width='1.5'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='bgblur_0_0_1_clip_path'%20transform='translate(247%20133.5)'%3e%3c/clipPath%3e%3clinearGradient%20id='paint0_linear_0_1'%20x1='12.8636'%20y1='6.75'%20x2='12.0304'%20y2='6.78541'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231B2B47'/%3e%3cstop%20offset='1'%20stop-color='%232D4877'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_0_1'%20x1='17.0909'%20y1='5.875'%20x2='12.2546'%20y2='11.6306'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231B2B47'/%3e%3cstop%20offset='1'%20stop-color='%232D4877'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

'%20stroke-width='1.5'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20id='Vector_2'%20d='M5%2012L12%2019L19%2012'%20stroke='url(%23paint1_linear_0_1)'%20stroke-width='1.5'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='bgblur_0_0_1_clip_path'%20transform='translate(816%20133)'%3e%3c/clipPath%3e%3clinearGradient%20id='paint0_linear_0_1'%20x1='12.8636'%20y1='17.25'%20x2='12.0304'%20y2='17.2146'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231B2B47'/%3e%3cstop%20offset='1'%20stop-color='%232D4877'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_0_1'%20x1='17.0909'%20y1='18.125'%20x2='12.2546'%20y2='12.3694'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231B2B47'/%3e%3cstop%20offset='1'%20stop-color='%232D4877'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

Callout

Even in the down scenario, the position stays open through the drop - Binaxity doesn't force-sell because of routine price movement. You choose when to exit. (A sustained decline can raise your variable interest rate rather than trigger a sale.)

YMYL note

Numbers are hypothetical and for illustration only. Not a guarantee of returns, not a commitment to lend. Gold prices move, and you may lose part or all of your contribution.

Why investors choose a Gold I-LOC with Binaxity

-

Double the buying power

Every dollar you contribute is matched one-to-one, so your gold position grows at twice the pace your own capital would allow - without selling other assets to fund it.

-

Bring cash, not collateral

You don't pledge anything. Any gold you already own stays yours and untouched; this is about building a new position, not borrowing against an old one.

-

Interest-only, no principal

While your position is open, you owe interest on the borrowed half and nothing more. No amortization schedule, no balloon, no surprise repayment date.

'/%3e%3cg%20id='vuesax/bold/trade_2'%3e%3cg%20id='trade'%3e%3cpath%20id='Vector'%20d='M7.3262%2024.9883H24.6758C24.8314%2024.9883%2024.9649%2025.1217%2024.9649%2025.2773C24.9647%2025.4329%2024.8314%2025.5664%2024.6758%2025.5664H7.3262C7.17074%2025.5663%207.03727%2025.4328%207.03714%2025.2773C7.03714%2025.1218%207.17067%2024.9884%207.3262%2024.9883ZM8.29007%2012.583H9.83206C10.1255%2012.583%2010.3623%2012.8159%2010.3623%2013.1133V21.4219C10.3622%2021.7123%2010.1225%2021.9521%209.83206%2021.9521H8.29007C7.9997%2021.952%207.75996%2021.7122%207.7598%2021.4219V13.1133C7.7598%2012.8228%207.99959%2012.5831%208.29007%2012.583ZM15.2295%209.50879H16.7715C17.0619%209.50882%2017.3016%209.74771%2017.3018%2010.0381V21.4219C17.3017%2021.7123%2017.062%2021.9521%2016.7715%2021.9521H15.2295C14.939%2021.9521%2014.6994%2021.7123%2014.6992%2021.4219V10.0381C14.6995%209.7477%2014.9391%209.50879%2015.2295%209.50879ZM22.17%206.43359H23.7119C24.0025%206.43359%2024.2422%206.67329%2024.2422%206.96387V21.4219C24.2421%2021.7124%2024.0025%2021.9521%2023.7119%2021.9521H22.17C21.8795%2021.952%2021.6398%2021.7123%2021.6397%2021.4219V6.96387C21.6397%206.67337%2021.8795%206.43372%2022.17%206.43359Z'%20fill='url(%23paint1_linear_0_1)'%20stroke='url(%23paint2_linear_0_1)'%20stroke-width='0.86747'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_0_1'%20x1='16'%20y1='32'%20x2='16'%20y2='0'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231F2937'/%3e%3cstop%20offset='1'%20stop-color='%231F2937'%20stop-opacity='0.68'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_0_1'%20x1='6.74812'%20y1='27.7833'%20x2='7.59908'%20y2='5.84042'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23D4A041'/%3e%3cstop%20offset='0.410355'%20stop-color='%23FBE67B'/%3e%3cstop%20offset='0.769917'%20stop-color='%23F7D14E'/%3e%3cstop%20offset='1'%20stop-color='%23D4A041'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_0_1'%20x1='16.0011'%20y1='5.47368'%20x2='16.0011'%20y2='26.5263'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='white'%20stop-opacity='0.2'/%3e%3cstop%20offset='1'%20stop-color='white'%20stop-opacity='0.01'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

'/%3e%3cg%20id='vuesax/bold/trade_2'%3e%3cg%20id='trade'%3e%3cpath%20id='Vector'%20d='M16%206.28027C21.3654%206.28027%2025.7197%2010.6346%2025.7197%2016C25.7197%2021.3654%2021.3654%2025.7197%2016%2025.7197C10.6346%2025.7197%206.28027%2021.3654%206.28027%2016C6.28027%2010.6346%2010.6346%206.28027%2016%206.28027ZM19.2695%2017.0996C18.2939%2017.0999%2017.5098%2017.8971%2017.5098%2018.8604C17.51%2019.8359%2018.3064%2020.6199%2019.2695%2020.6201C20.2441%2020.6201%2021.0301%2019.8348%2021.0303%2018.8604C21.0303%2017.8845%2020.2329%2017.0996%2019.2695%2017.0996ZM19.5977%2011.9922C19.1983%2011.5929%2018.5409%2011.5929%2018.1416%2011.9922L11.5918%2018.542C11.1926%2018.9413%2011.1926%2019.5987%2011.5918%2019.998C11.7971%2020.2033%2012.0601%2020.2998%2012.3203%2020.2998C12.5804%2020.2997%2012.8427%2020.2032%2013.0479%2019.998L19.5977%2013.4482C19.997%2013.0489%2019.997%2012.3915%2019.5977%2011.9922ZM12.7305%2011.3799C11.7559%2011.3799%2010.9699%2012.1652%2010.9697%2013.1396C10.9697%2014.1155%2011.7671%2014.9004%2012.7305%2014.9004C13.7061%2014.9001%2014.4902%2014.1029%2014.4902%2013.1396C14.49%2012.1641%2013.6935%2011.3801%2012.7305%2011.3799Z'%20fill='url(%23paint1_linear_0_1)'%20stroke='url(%23paint2_linear_0_1)'%20stroke-width='0.56'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_0_1'%20x1='16'%20y1='32'%20x2='16'%20y2='0'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231F2937'/%3e%3cstop%20offset='1'%20stop-color='%231F2937'%20stop-opacity='0.68'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_0_1'%20x1='6.42088'%20y1='24.009'%20x2='24.2115'%20y2='8.09269'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23D4A041'/%3e%3cstop%20offset='0.410355'%20stop-color='%23FBE67B'/%3e%3cstop%20offset='0.769917'%20stop-color='%23F7D14E'/%3e%3cstop%20offset='1'%20stop-color='%23D4A041'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_0_1'%20x1='16'%20y1='5.47368'%20x2='16'%20y2='26.5263'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='white'%20stop-opacity='0.2'/%3e%3cstop%20offset='1'%20stop-color='white'%20stop-opacity='0.01'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

-

Accumulate on your own terms

Contribute steadily, pause when you need to, scale up as your conviction grows. The credit line flexes around your schedule, not the other way around.

-

A potentially tax-smart approach

Building a position through a credit line - rather than selling existing holdings to fund a gold purchase - may help you avoid some taxable events. Individual circumstances vary; consult a qualified tax advisor.

-

Tokenized gold in digital-asset custody

Your position is held as XAUt - a token designed to represent ownership of physical gold - secured in Binaxity's digital-asset custody with wallet-level MPC controls, with full dashboard visibility. The physical gold backing is managed through the XAUt issuer's reserve and custodian structure.

-

No volatility-driven margin calls

There are no LTV thresholds and no automatic sales triggered by market swings. A falling price lowers your position's value but doesn't force an exit - the single biggest risk in collateralized gold lending isn't part of the structure.

'/%3e%3cg%20id='vuesax/bold/trade_2'%3e%3cg%20id='trade'%3e%3cpath%20id='Vector'%20d='M16%206.375C21.3129%206.375%2025.625%2010.6871%2025.625%2016C25.625%2021.3129%2021.3129%2025.625%2016%2025.625C10.6871%2025.625%206.37503%2021.3129%206.37503%2016C6.37503%2010.6871%2010.6871%206.375%2016%206.375ZM20.8233%2015.5391C20.1926%2015.449%2019.6385%2015.8872%2019.5489%2016.4941C19.43%2017.2899%2019.0846%2017.9956%2018.545%2018.5352C17.6029%2019.4771%2016.2693%2019.7854%2015.0684%2019.4609C15.3944%2019.263%2015.6153%2018.9059%2015.6153%2018.5C15.6153%2017.883%2015.1073%2017.3751%2014.4903%2017.375H11.8203C11.2032%2017.375%2010.6953%2017.8829%2010.6953%2018.5V21.1699C10.6953%2021.787%2011.2032%2022.2949%2011.8203%2022.2949C12.4373%2022.2948%2012.9453%2021.7869%2012.9453%2021.1699V20.957C13.8763%2021.538%2014.9328%2021.8447%2016%2021.8447C17.4948%2021.8447%2018.9912%2021.2783%2020.1348%2020.1348C21.0241%2019.2455%2021.5899%2018.1013%2021.7813%2016.8154L21.7823%2016.8057C21.8561%2016.2004%2021.4425%2015.6295%2020.8242%2015.5391H20.8233ZM20.17%209.69531C19.5529%209.69536%2019.045%2010.2032%2019.045%2010.8203V11.0449C16.801%209.65583%2013.8201%209.91915%2011.8653%2011.8643L11.8633%2011.8662C10.9764%2012.7638%2010.41%2013.9076%2010.2285%2015.1758C10.1391%2015.7874%2010.5684%2016.3648%2011.1719%2016.4424V16.4404C11.2417%2016.4533%2011.297%2016.4551%2011.3301%2016.4551C11.8819%2016.455%2012.3655%2016.052%2012.4414%2015.4902L12.4405%2015.4893C12.5602%2014.6959%2012.9071%2013.9933%2013.4453%2013.4551C14.387%2012.5135%2015.7194%2012.2055%2016.92%2012.5293C16.5947%2012.7274%2016.375%2013.0849%2016.375%2013.4902C16.3752%2014.1072%2016.883%2014.6152%2017.5%2014.6152H20.17C20.787%2014.6152%2021.2948%2014.1072%2021.295%2013.4902V10.8203C21.295%2010.2032%2020.7871%209.69531%2020.17%209.69531Z'%20fill='url(%23paint1_linear_0_1)'%20stroke='url(%23paint2_linear_0_1)'%20stroke-width='0.749975'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_0_1'%20x1='16'%20y1='32'%20x2='16'%20y2='0'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231F2937'/%3e%3cstop%20offset='1'%20stop-color='%231F2937'%20stop-opacity='0.68'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_0_1'%20x1='6.00003'%20y1='26'%20x2='27.2516'%20y2='18.6309'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23D4A041'/%3e%3cstop%20offset='0.410355'%20stop-color='%23FBE67B'/%3e%3cstop%20offset='0.769917'%20stop-color='%23F7D14E'/%3e%3cstop%20offset='1'%20stop-color='%23D4A041'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_0_1'%20x1='16'%20y1='5.47368'%20x2='16'%20y2='26.5263'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='white'%20stop-opacity='0.2'/%3e%3cstop%20offset='1'%20stop-color='white'%20stop-opacity='0.01'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

'/%3e%3cg%20id='vuesax/bold/trade_2'%3e%3cg%20id='trade'%3e%3cpath%20id='Vector'%20d='M12.0723%206.28027H16.3116C16.7069%206.28027%2017.0323%206.60464%2017.0323%207V9.88965C17.0323%2012.4143%2019.0877%2014.4697%2021.6123%2014.4697H24.502C24.8973%2014.4697%2025.2217%2014.7951%2025.2217%2015.1904V20.4297C25.2217%2022.1459%2024.6257%2023.4619%2023.6807%2024.3496C22.7328%2025.2399%2021.4117%2025.7197%2019.9317%2025.7197H12.0723C10.5923%2025.7197%209.2712%2025.2399%208.32327%2024.3496C7.37825%2023.4619%206.78226%2022.1459%206.78226%2020.4297V11.5703C6.78226%209.85414%207.37825%208.53809%208.32327%207.65039C9.2712%206.76009%2010.5923%206.28027%2012.0723%206.28027ZM11.502%2019.9697C10.9373%2019.9697%2010.4717%2020.4354%2010.4717%2021C10.4717%2021.5646%2010.9373%2022.0303%2011.502%2022.0303H15.502C16.0666%2022.0303%2016.5323%2021.5646%2016.5323%2021C16.5323%2020.4354%2016.0666%2019.9697%2015.502%2019.9697H11.502ZM11.502%2015.9697C10.9373%2015.9697%2010.4717%2016.4354%2010.4717%2017C10.4717%2017.5646%2010.9373%2018.0303%2011.502%2018.0303H17.502C18.0666%2018.0303%2018.5323%2017.5646%2018.5323%2017C18.5323%2016.4354%2018.0666%2015.9697%2017.502%2015.9697H11.502ZM18.9619%206.65039C18.9619%206.3472%2019.3576%206.16223%2019.6035%206.4082C21.0831%207.88773%2023.6616%2010.4963%2025.1026%2011.9473L25.1035%2011.9482C25.3106%2012.1554%2025.1757%2012.5397%2024.8321%2012.54C23.7015%2012.54%2022.3828%2012.5403%2021.4346%2012.5303H21.4317C20.0689%2012.5303%2018.9619%2011.4377%2018.9619%2010.1396V6.65039Z'%20fill='url(%23paint1_linear_0_1)'%20stroke='url(%23paint2_linear_0_1)'%20stroke-width='0.56'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_0_1'%20x1='16'%20y1='32'%20x2='16'%20y2='0'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231F2937'/%3e%3cstop%20offset='1'%20stop-color='%231F2937'%20stop-opacity='0.68'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_0_1'%20x1='6.90182'%20y1='24.009'%20x2='24.5687'%20y2='8.99369'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23D4A041'/%3e%3cstop%20offset='0.410355'%20stop-color='%23FBE67B'/%3e%3cstop%20offset='0.769917'%20stop-color='%23F7D14E'/%3e%3cstop%20offset='1'%20stop-color='%23D4A041'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_0_1'%20x1='16.002'%20y1='5.47368'%20x2='16.002'%20y2='26.5263'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='white'%20stop-opacity='0.2'/%3e%3cstop%20offset='1'%20stop-color='white'%20stop-opacity='0.01'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

'/%3e%3cg%20id='vuesax/bold/trade_2'%3e%3cg%20id='trade'%3e%3cpath%20id='Vector'%20d='M14.1211%206.57715C15.2459%206.11835%2016.5059%206.08964%2017.6475%206.49121L17.8741%206.57715L23.4463%208.8584H23.4473C23.7854%208.99452%2024.1027%209.27319%2024.336%209.62012C24.5692%209.96706%2024.707%2010.3647%2024.7071%2010.7246V15.1172C24.707%2019.762%2021.4357%2024.1323%2016.8994%2025.5977L16.4571%2025.7295C16.2%2025.7996%2015.9216%2025.8084%2015.6592%2025.7559L15.5479%2025.7295C10.7834%2024.413%207.29794%2019.9116%207.29788%2015.1172V10.7246C7.29795%2010.3647%207.43582%209.96726%207.668%209.62012C7.90027%209.27288%208.21472%208.99432%208.54788%208.8584L14.1211%206.57715ZM16.002%2011.7852C14.5054%2011.7854%2013.291%2013.0005%2013.291%2014.4971C13.2912%2015.6487%2014.0245%2016.6266%2015.042%2017.0146V19.499C15.042%2020.0251%2015.4759%2020.4597%2016.002%2020.46C16.5282%2020.46%2016.9629%2020.0253%2016.9629%2019.499V17.0156C17.9801%2016.6286%2018.7138%2015.6587%2018.7139%2014.4971C18.7139%2013.0003%2017.4987%2011.7852%2016.002%2011.7852Z'%20fill='url(%23paint1_linear_0_1)'%20stroke='url(%23paint2_linear_0_1)'%20stroke-width='0.42021'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_0_1'%20x1='16'%20y1='32'%20x2='16'%20y2='0'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231F2937'/%3e%3cstop%20offset='1'%20stop-color='%231F2937'%20stop-opacity='0.68'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_0_1'%20x1='7.46311'%20y1='24.009'%20x2='24.9156'%20y2='10.0902'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23D4A041'/%3e%3cstop%20offset='0.410355'%20stop-color='%23FBE67B'/%3e%3cstop%20offset='0.769917'%20stop-color='%23F7D14E'/%3e%3cstop%20offset='1'%20stop-color='%23D4A041'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_0_1'%20x1='16.0024'%20y1='5.47368'%20x2='16.0024'%20y2='26.5263'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='white'%20stop-opacity='0.2'/%3e%3cstop%20offset='1'%20stop-color='white'%20stop-opacity='0.01'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

'/%3e%3cg%20id='vuesax/bold/trade_2'%3e%3cg%20id='trade'%3e%3cpath%20id='Vector'%20d='M16.0117%206.22754C16.3645%206.22755%2016.7038%206.27651%2016.9483%206.36621V6.36719L22.4473%208.42578V8.42676C22.9089%208.60272%2023.3437%208.97065%2023.6631%209.43457C23.9826%209.89876%2024.1714%2010.4365%2024.167%2010.9326V19.0352C24.1669%2019.3849%2024.0499%2019.8095%2023.8496%2020.21C23.6494%2020.6103%2023.3789%2020.9589%2023.0977%2021.1709L17.5987%2025.2803V25.2812C17.1707%2025.6033%2016.5926%2025.7724%2016.002%2025.7725C15.4114%2025.7725%2014.8333%2025.6033%2014.4053%2025.2812L14.4043%2025.2803L8.90433%2021.1709L8.90335%2021.1699L8.79886%2021.0859C8.55734%2020.8757%208.32875%2020.5656%208.15335%2020.2139C7.9531%2019.8122%207.83703%2019.3852%207.83694%2019.0352V10.9346C7.83699%2010.4376%208.0278%209.89979%208.34964%209.43555C8.63129%209.02934%209.00148%208.69679%209.40237%208.50195L9.57523%208.42676L15.0742%206.36621C15.3188%206.27634%2015.6586%206.22754%2016.0117%206.22754ZM19.6944%2012.4971C19.295%2012.0977%2018.6377%2012.0977%2018.2383%2012.4971L14.666%2016.0684L13.7842%2015.1865C13.3849%2014.7876%2012.7284%2014.7876%2012.3291%2015.1865C11.9304%2015.5853%2011.9296%2016.2411%2012.3272%2016.6406V16.6416L13.9278%2018.2617L13.9287%2018.2627C14.1339%2018.4679%2014.3962%2018.5644%2014.6563%2018.5645C14.9165%2018.5645%2015.1795%2018.468%2015.3848%2018.2627L19.6846%2013.9629L19.6836%2013.9619C20.0936%2013.562%2020.0932%2012.8959%2019.6944%2012.4971Z'%20fill='url(%23paint1_linear_0_1)'%20stroke='url(%23paint2_linear_0_1)'%20stroke-width='0.56'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_0_1'%20x1='16'%20y1='32'%20x2='16'%20y2='0'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%231F2937'/%3e%3cstop%20offset='1'%20stop-color='%231F2937'%20stop-opacity='0.68'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_0_1'%20x1='7.9121'%20y1='24.0508'%20x2='25.1975'%20y2='11.0594'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23D4A041'/%3e%3cstop%20offset='0.410355'%20stop-color='%23FBE67B'/%3e%3cstop%20offset='0.769917'%20stop-color='%23F7D14E'/%3e%3cstop%20offset='1'%20stop-color='%23D4A041'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_0_1'%20x1='16.0017'%20y1='5.41819'%20x2='16.0017'%20y2='26.5813'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='white'%20stop-opacity='0.2'/%3e%3cstop%20offset='1'%20stop-color='white'%20stop-opacity='0.01'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

Rates & terms

- 6.5%

Annual Percentage Rate (APR)

Starting rate (adjustable based on market conditions) - $10

Minimum investment

Max $10,000 combined across all I-LOC assets

Interest is charged on the borrowed portion only and is variable (see "How your rate works"). No origination fee at opening, no closing fee, no top-up fee, no inactivity fee.

How your rate works

Your interest applies to the borrowed half of your position only - your own contribution never accrues interest. The rate is variable, reviewed daily, and set from several factors: the asset type, your borrower profile, market liquidity, gold's volatility, and the gap between gold's current price and the reference price at your drawdown.

In plain terms: if gold falls materially below your reference price, the applicable rate can rise to reflect the higher risk on your position. A larger decline can mean a higher rate on your outstanding balance - but a price drop on its own never triggers an automatic sale or margin call, as long as your account stays in good standing and interest payments are current.

Illustrative Rate Schedule

(by how far gold sits below your reference price)

| Decline from reference price | Illustrative rate (per annum) |

|---|---|

| Less than 25% | 6.5% |

| 25% to <40% | 7.5% |

| 40% to <50% | 8.5% |

| 50% to <60% | 9.5% |

| 60% to <70% | 10.5% |

| 70% to <80% | 12.5% |

| 80% or more | 15.5% |

Illustrative only. Actual rates depend on live conditions and product terms.

Security & custody

Your gold position is held as XAUt, a token designed to represent ownership of physical gold.

There are two layers to how it's secured:

The token layer (Binaxity)

Binaxity holds your XAUt in its digital-asset custody infrastructure, with wallet-level MPC controls - key material is split so no single party holds complete signing authority.

You can see your token balances in your dashboard at any time.

The physical-gold layer (issuer)

The physical gold backing XAUt is held through the XAUt issuer's custodian arrangement - Binaxity does not operate a bullion vault itself.

Reserve reports, insurance, segregation, and audit/attestation of the physical backing are issuer-level matters, based on the XAUt issuer's disclosures and reserve reporting.

All transactions run through standard KYC/AML and on-chain monitoring. XAUt is acquired through approved digital-asset venues or liquidity counterparties.

- Digital-asset custody with MPC controls

- XAUt token balances visible 24/7

- Issuer reserve reports & attestation

- KYC/AML compliance

- Physical backing via XAUt issuer's custodian structure

- Acquisition via approved venues

Who can open a Gold Investment Line of Credit

A Gold Investment Line of Credit is available in select jurisdictions only. A number of countries are restricted for regulatory, legal, or compliance reasons, and the list can change - check eligibility before applying.

Requirements

- Meet KYC requirements including valid government-issued ID and identity verification

- Eligible jurisdiction

- Co-investment in stablecoins (USDC / USDT)

- Minimum investment: $10 (max $10,000 combined across all I-LOC assets)

Key restricted jurisdictions include:

- United States of America

- Canada

- People's Republic of China

- Cayman Islands

- Russia, Ukraine, Iran, North Korea, and many others

The full restricted jurisdictions list is extensive. Check the complete list before applying.

Apply nowFrequently asked questions

-

A Gold I-LOC is a credit facility designed to help you build gold exposure over time through a 1:1 matched structure. You contribute capital, Binaxity matches it with credit, and the combined amount is used to acquire tokenized gold for your position.

Unlike a traditional gold loan where you pledge bullion you already own, Binaxity's Gold I-LOC is designed for accumulation. It helps you build gold exposure using disciplined, asset-building credit rather than borrowing against existing gold.

-

You start by applying through Binaxity's onboarding flow. After providing the required information, Binaxity reviews your application and assigns an approved credit limit, subject to eligibility, product availability, and signing the applicable agreement when taking out a loan.

Once approved, you can choose when to draw from your credit line, how much to draw, and how often to use it, subject to your available limit.

-

No. Binaxity's Gold I-LOC is not designed around borrowing against gold you already own.

Instead, you contribute stablecoin funding such as USDC or USDT, Binaxity matches your contribution with credit, and the combined amount is used to acquire tokenized gold for your vault.

-

With Binaxity's Gold I-LOC, your position is represented through tokenized gold, not physical bullion delivered directly to you.

The tokenized gold is designed to track gold exposure and is shown in your Binaxity vault dashboard. You do not take possession of physical gold bars or coins through the Gold I-LOC.

-

The minimum investment to get started with Binaxity's Gold I-LOC starts at $10.

You can begin with a smaller amount and build your gold position over time, rather than needing a large upfront investment.

-

Gold price movement does not automatically trigger a margin call or forced liquidation under Binaxity's Gold I-LOC.

Your monthly interest obligation remains based on your outstanding loan principal. As long as your payments remain current and you comply with your agreement, your position is not automatically sold just because the market price drops.

That said, gold and tokenized gold can fluctuate in value, and your position can go down. You should only participate if you understand the risks.

-

Each drawdown is structured as its own interest-only loan. This means you make monthly interest payments on the outstanding loan principal, while principal repayment is not required during the term unless you redeem or otherwise settle the loan.

If you have multiple active drawdowns, Binaxity may consolidate your monthly payment view to make repayment easier to manage.

-

Yes. If you have available credit, you can make additional drawdowns over time to increase your gold exposure.

Each drawdown uses the same 1:1 matched structure: you contribute capital, Binaxity matches it with credit, and the combined amount is used to acquire additional tokenized gold for your vault.

-

You can request to close your Gold I-LOC by redeeming your gold position, subject to the terms of your loan agreement and completion of Binaxity's processing checks.

When you redeem, the proceeds are first used to repay any outstanding loan balance. Any remaining net proceeds are paid out to you.

The Compound View

Insights on credit, investing, and modern wealth-building. Demystifying how structured borrowing and smart portfolio strategies can work for you.

Start building your gold position today

Most credit products are built for spending. A Gold Investment Line of Credit is built for the opposite - a structured way to accumulate more gold over time, on your own schedule.

Apply now