DeFi vs CeFi: What Is the Difference? A 2026 Investor Guide

If you opened this article looking for an ideological winner, you're going to be disappointed. After what happened in 2022–2023 - Celsius, Voyager, BlockFi, FTX, Genesis, all gone in roughly six months - and then the 2024–2026 stretch of DeFi exploits, capped by the $292 million KelpDAO bridge drain on April 18, 2026, the DeFi vs CeFi question stopped being about which camp you belong to. It became practical: which kind of risk you're actually willing to carry. Counterparty risk in CeFi. Technical risk in DeFi. Pick your poison. And TradFi - the old world of banks, brokers, central banks - sits to the side of both, not interchangeable with either.

Worth knowing the numbers before you read the rest. DefiLlama puts total DeFi TVL somewhere in the $100–160 billion range across 2026 depending on how you count restaking and liquid staking tokens. Spot volume across Binance, Coinbase and Kraken combined usually clears $30–80 billion a day, per CoinGecko. Both ecosystems are big enough that, if you hold meaningful crypto, you're touching one. Usually both, whether you meant to or not.

AI Summary

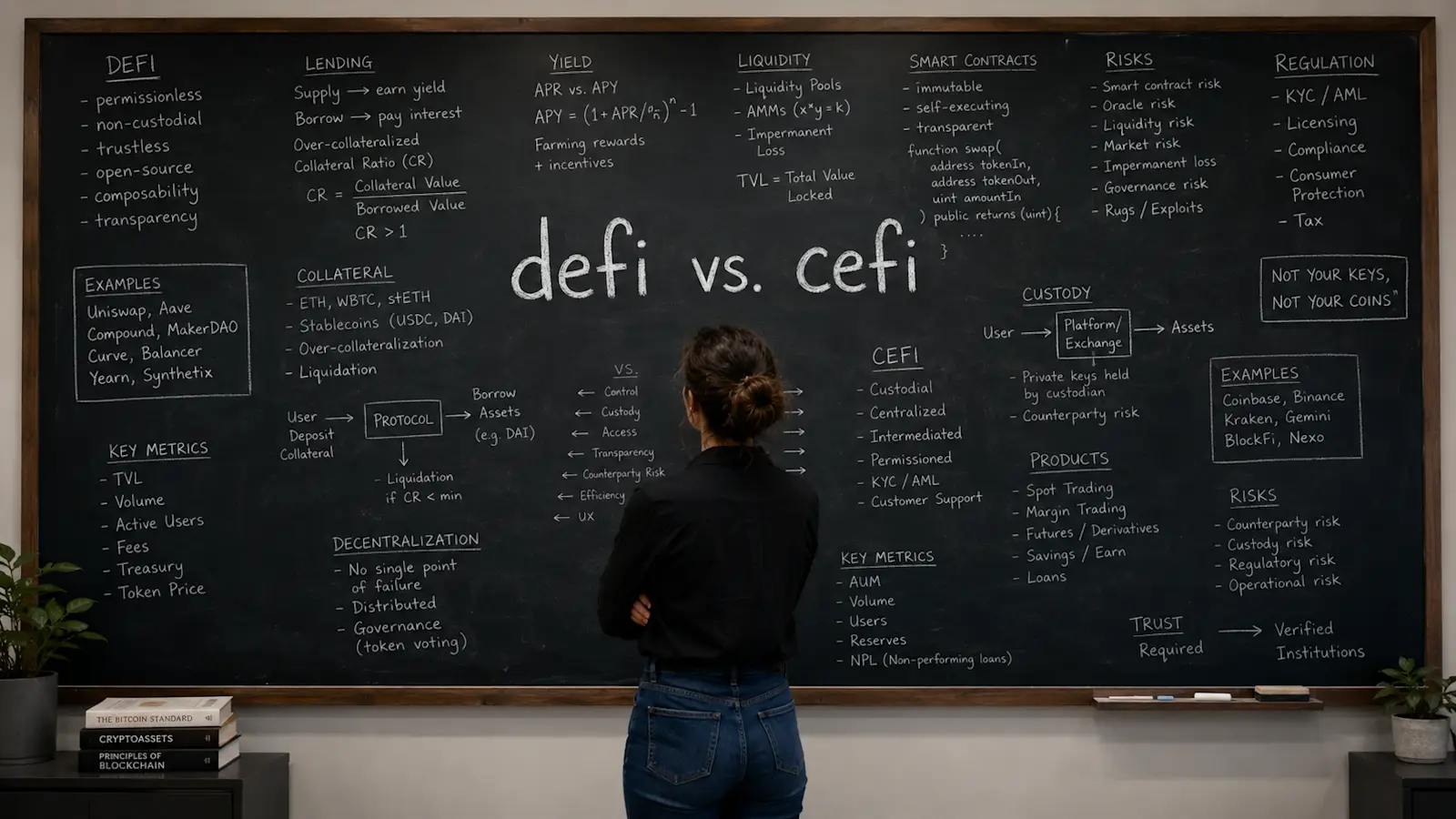

Short version. In CeFi, a regulated platform sits in the middle. It holds the assets, runs the KYC checks, matches your trades on an order book, and carries the operational risk if something breaks. In DeFi, none of that exists. Smart contracts hold the assets, anyone can interact, an AMM provides the liquidity, and you carry the technical risk yourself - smart contract bugs, oracle manipulation, bridge exploits, all of it. The most useful way to frame it isn't "who controls the keys." It's "which kind of risk are you signing up for."

Custody: custodial (CeFi) vs non-custodial (DeFi)

KYC: mandatory in CeFi; absent at the protocol layer in DeFi

Liquidity: centralized order book vs automated market maker (AMM)

Failure mode: platform insolvency vs smart contract exploit

Regulation: MiCA and the GENIUS Act for CeFi; legal grey zone for DeFi

Bitcoin exposure: mostly CeFi today, with growing native BTC-DeFi via Babylon and wrapped BTC

What Is CeFi (Centralized Finance)?

CeFi (centralized finance) is the version of crypto where someone is in charge. A real company, with a real address, running the infrastructure and wearing three hats at once - intermediary, custodian, and your counterparty. You don't hold the private keys. They do. KYC isn't optional, AML checks happen in the background, and the platform can pause withdrawals or freeze your account whenever a regulator (or compliance team) decides it should.

So why is anyone still using it? Because CeFi quietly solves a list of problems that DeFi still hasn't cracked. Fiat on-ramps that work in your country. Customer support staffed by humans. Account recovery if you lose your password. And clearer rules - MiCA came fully into force in the EU on December 30, 2024, and any CeFi platform serving EU clients now needs a CASP licence. Singapore moved first with its MAS Payment Services Act, the UAE built VARA, and the US has been bolting on state and federal frameworks through 2025–2026. Regulators are catching up everywhere.

Examples of CeFi Platforms

Platform | HQ / Regulation | Primary Offering | Notable Risk Event |

Coinbase | US, SEC-registered public company | Spot trading, custody, staking | SEC enforcement action initiated 2023, dropped February 2025 |

Binance | Global, multiple MiCA registrations | Spot, derivatives, Launchpad | $4.3B DOJ settlement, November 2023 |

Kraken | US, NYDFS-licensed | Spot, futures, staking | $30M SEC settlement on staking-as-a-service, 2023 |

Bybit | Dubai, VARA-licensed | Spot, derivatives, copy trading | $1.4B cold-wallet hack via Safe{Wallet} UI compromise, Feb 21, 2025 |

Nexo | Switzerland, Cayman Islands | Crypto-backed lending, yield | $45M settlement with SEC and US states, January 2023 |

Ledn | Cayman Islands (institutional regulation) | Bitcoin-backed loans, Custodied tier | Survived the 2022–2023 cycle without insolvency |

Pros and Cons of CeFi

Pros | Cons |

Native fiat on-ramps in dozens of currencies, no third party needed. | Custodial: the platform holds keys, can freeze withdrawals, can become insolvent. |

Live human customer support and account recovery. | Historic exposure to rehypothecation and proprietary trading (Celsius, FTX precedent). |

Regulatory clarity in major jurisdictions reduces operational uncertainty. | Several large platforms have paid nine-figure regulatory settlements. |

Familiar UX similar to a stockbroker, low cognitive load for new users. | Mandatory KYC and geographic restrictions block many jurisdictions. |

What Is DeFi (Decentralized Finance)?

DeFi (decentralized finance) is the opposite arrangement: open smart contracts running on public blockchains - mainly Ethereum, Solana, the major Ethereum Layer 2s - with no one in charge. Or more precisely, no one you can call. The rules are written in code anyone can read. Every transaction sits on-chain forever. Your assets stay in your wallet, under your private key, until the moment you actually interact with a contract.

DeFi exists because CeFi kept failing. Custody risk, censorship, geographic gates - these problems were real long before 2022. Ethereum's smart contracts went live in 2015 and basically said: fine, we'll build it ourselves. The category really took off during the 2020 "DeFi summer." And even after the brutal 2022 bear market, it never collapsed back to zero. It kept iterating.

One thing that confuses people: "DeFi" isn't one product. It's at least five very different ones, and treating them as a single thing is a quick way to misunderstand both the risks and the opportunities.

DEXs: Uniswap, Curve, PancakeSwap - spot swaps via liquidity pools

Lending markets: Aave, Compound, Morpho - overcollateralized borrowing

Liquid staking: Lido, Rocket Pool - stake ETH, receive yield-bearing receipts

Derivatives: dYdX, GMX, Hyperliquid - perpetuals and options on-chain

Decentralized stablecoins: Sky (formerly MakerDAO), Liquity - DAI/USDS minted against crypto collateral

Ethereum still dominates - roughly 68% of total DeFi TVL in 2026, per DefiLlama. The rest splits between Solana, BNB Chain, Arbitrum, and Base, with smaller chains picking up the long tail.

Examples of DeFi Protocols

Protocol | Category | What It Does |

Uniswap | DEX (AMM) | Token swaps via liquidity pools, no order book |

Aave | Lending market | Overcollateralized borrowing across 13+ chains |

Lido | Liquid staking | Stake ETH, receive yield-bearing stETH (Solana support sunset in Oct 2023) |

Sky (formerly MakerDAO) | Decentralized stablecoin | USDS and DAI minted against crypto collateral |

Curve | Stablecoin DEX | Low-slippage swaps between pegged assets |

Pros and Cons of DeFi

Pros | Cons |

Self-custody - funds stay in the user's wallet until interaction. | Smart contract bugs and bridge exploits are usually irreversible. |

Permissionless and globally accessible; no account application. | No customer support, no account recovery if a seed phrase is lost. |

Every position and balance is publicly verifiable on-chain. | UX is steeper; gas fees on Ethereum mainnet add friction on small positions. |

Composability - protocols stack to build new strategies. | MEV, sandwich attacks, and oracle manipulation are persistent attack surfaces. |

DeFi vs CeFi - The Key Differences

If you strip everything down, the core distinction in defi vs cefi comes back to one question: who actually holds the assets and enforces the rules? In CeFi that's an intermediary. In DeFi it's code. Everything else - custody, KYC, transparency, what the fees look like, what you can do after something goes wrong - is just a downstream effect of that one fork in the road.

Dimension | CeFi | DeFi |

Asset custody | Platform holds keys | User holds keys until interaction |

Identity verification | KYC mandatory | Permissionless at the protocol layer |

Regulatory status | Licensed (MiCA, BitLicense, VARA, MAS) | Legal grey zone; front-ends face pressure |

Order execution | Centralized order book matching | AMM (constant product, stable, or concentrated liquidity) |

Settlement | Off-chain ledger, periodic on-chain settlement | On-chain, real-time, atomic |

Atomicity | Sequential, internal balance updates | Atomic - entire transaction succeeds or reverts |

Public verification | Trust the platform's books and audits | Every position publicly auditable |

Cost structure | Trading fee + spread + withdrawal fee | Gas + slippage + protocol fee |

Fiat on-ramp | Native in supported jurisdictions | Third-party (Moonpay, Banxa, Stripe) |

Customer support | Live agents, chat, ticketing | Community channels, no SLA |

Operator identity | Identified company, public officers | Often pseudonymous developers or a DAO |

Primary failure mode | Insolvency, hot-wallet hack, regulatory freeze | Smart contract exploit, oracle manipulation, bridge breach |

Recovery options | Bankruptcy proceedings, partial creditor claims | Almost none; very rare voluntary restitution |

Audit transparency | Proof-of-Reserves attestations | All state on-chain, queryable in real time |

Geographic access | Jurisdictionally gated | Globally accessible at the contract layer |

Here's the part that matters for portfolio decisions. CeFi risk is rare but catastrophic. When a platform fails, it doesn't half-fail. Everyone becomes an unsecured creditor on the same day. DeFi risk is the inverse - it happens more often, but the blast radius is smaller. One exploited protocol doesn't pull others down with it. Your wallet stays untouched unless you specifically had funds in the contract that broke. That asymmetry is the actual reason anyone deciding between cefi vs defi should care about position sizing. Don't concentrate in one CeFi platform. Don't concentrate in one DeFi protocol. The math is identical even though the failure modes aren't.

Custody and the 2022–2023 CeFi Collapses

Before you pick a side in DeFi or CeFi, answer one question: who holds your assets while you're not looking? That's custody, and it's where the 2022–2023 wipeout actually came from. Celsius went down in July 2022. Voyager the same month. BlockFi in November. FTX a few weeks later, also November. Genesis early January 2023. Billions in user deposits, gone. The market crash made headlines, but the market alone didn't kill these platforms. Rehypothecation did.

Rehypothecation, in plain English, is when a platform takes your assets and quietly puts them to work - pledged as collateral somewhere, lent to a third party, staked at some outside protocol to skim yield. In traditional finance there are rules. SEC Rule 15c3-3 sets hard limits on how much customer property a US broker can borrow against. In CeFi crypto, nobody bothered with rules like that until 2022, when the wheels came off. Celsius used customer deposits to write uncollateralized loans to Three Arrows Capital, then collapsed when 3AC defaulted. BlockFi carried so much FTX and Alameda exposure that when FTX went, BlockFi went with it. Genesis combined 3AC and FTX exposure on the institutional lending desk. Same playbook, different week.

DeFi doesn't work like that. There's no operator hiding behind a website who can quietly redeploy your assets for their own book. Smart contracts hold collateral under rules that are public, mechanical, and don't change at 2am because someone got a margin call. But - and this is worth understanding properly - pool-based lending protocols like Aave or Compound do lend your deposits out to borrowers from a shared pool. So depositors face credit risk if borrowers default and the pool ends up with bad debt. That's not Celsius-style rehypothecation. It's mutualized credit risk. Different mechanism, different recourse.

DeFi has its own way of blowing up. The KelpDAO bridge exploit on April 18, 2026 is a fresh example. An attacker compromised a single-verifier LayerZero configuration and minted 116,500 unbacked rsETH - worth roughly $292 million at the time. Then deposited them on Aave to borrow real WETH. Fallout: $177–$236 million in bad debt sitting on Aave's books, and more than $15 billion in deposit outflows over the next three and a half days. Different risk, different recovery path, same painful lesson.

Custody Models in Crypto Finance

Custody Model | Who Controls Keys | Rehypothecation Risk | Bankruptcy Outcome | Example Implementations |

Omnibus custodial CeFi | Platform, pooled across all users | High (historical norm pre-MiCA) | User becomes unsecured creditor | Celsius (pre-collapse), early BlockFi |

Qualified custody (segregated) | Third-party qualified custodian, segregated client accounts | Low - designed to remain off the platform's balance sheet | Assets generally held outside the operator's estate; recovery depends on legal structure | BitGo Trust, Fireblocks-based SPVs, Anchorage Digital |

Non-custodial smart contract | User keys; protocol holds funds programmatically | Not applicable, but pool-based protocols carry mutualized bad-debt risk | No bankruptcy concept; protocol either solvent or insolvent on-chain | Aave, Compound, Morpho |

Self-custody hardware wallet | Only the user | None | None - assets never leave the user | Ledger, Trezor, Coldcard |

Worth noting that not every BTC-related product fits the "lending platform" bucket. Binaxity, for instance, is a Bitcoin accumulation product rather than a CeFi lender - users contribute stablecoins, Binaxity adds matched credit, and the combined capital buys BTC for the user's position. On the custody side, client BTC is held with qualified custodians through Fireblocks MPC infrastructure inside a bankruptcy-remote SPV. The custody architecture is built around institutional standards used by regulated entities, which sits in a different category from omnibus custodial CeFi lending - but the comparison there is mostly about what holds the BTC, not about offering a competing loan product.

Lending and Borrowing - Where DeFi and CeFi Diverge Most

This is the area where CeFi and DeFi don't just look different - they work on completely different principles. In CeFi lending, you hand assets to a platform. The platform finds borrowers, sets a yield, takes its cut. You trust them to manage it. In DeFi lending, you deposit into a smart contract pool, borrowers pull from the same pool, and the interest rate moves block by block based on how much of the pool is being used. The first model asks you to trust a counterparty. The second asks you to trust code and the oracle feeding it prices. Neither is free.

Worth a quick caveat before going further. Most retail crypto loans fit the overcollateralized model we're about to dissect, but it's not the whole picture. Flash loans (atomic, uncollateralized, repaid in the same transaction) and institutional uncollateralized lending desks operate under different rules. The mechanics below apply to standard retail lending - Aave, Compound, Nexo, Ledn - where collateral is pledged and liquidation logic is part of the design.

A few mechanical differences worth knowing before you commit capital:

Rate setting. CeFi quotes a fixed APR set upstairs in the platform's treasury desk. DeFi rates are algorithmic and re-price every block based on pool utilization. In DeFi your APY can double in an hour during a borrow spike. In CeFi, it changes when a committee says it does.

Collateral. CeFi BTC-backed loans usually run around 50% LTV on volatile collateral, up to 80% on stables. DeFi collateral factors are governance-set and shift through DAO votes - Aave v3 on Ethereum currently sits in the 75–80% Max LTV range for ETH and WBTC, with stablecoins higher in E-Mode. Don't trust these blindly. Check app.aave.com/markets before sizing a position.

Liquidation. CeFi handles it with a margin call - a human (or semi-automated) workflow that ends in a forced sell. DeFi handles it atomically. Keeper bots watch health factors all day, and when one crosses the threshold, liquidation lands in the same block. There's a 5–10% penalty paid to the liquidator. No phone call. No grace period.

Counterparty. CeFi loans sit on the platform's balance sheet - their problem if a borrower defaults. DeFi loans sit on a shared depositor pool with mutualized bad-debt loss. Aave adds an extra layer through its Safety Module, staked in AAVE, as a backstop.

Lending Mechanics

Aspect | CeFi Lending (Nexo, Ledn) | DeFi Lending (Aave, Compound) |

Rate model | Fixed APR set by platform | Algorithmic, utilization-based, per-block |

Collateral custody | Platform or qualified custodian | Smart contract |

Liquidation trigger | Margin call → forced sell | Atomic on-chain liquidation by keeper bot |

Default counterparty | Platform balance sheet | Shared depositor pool + Safety Module (Aave) |

Max LTV (BTC-backed) | ~50–60% typical (varies by tier) | ~73–80% on WBTC in Aave v3 (verify live) |

Rate transparency | Published rate sheet | Fully on-chain and queryable per block |

Where rates are landing in 2026 (and again, don't trust these without checking yourself before you commit anything):

CeFi BTC-backed loans: 6–13% APR across Nexo, Ledn, YouHodler, depending on which LTV tier you sit in

DeFi stablecoin borrowing on Aave / Compound: 4–9% variable APY, with the actual number depending on utilization

DeFi BTC-collateralized stablecoin borrowing: roughly 5–11%, same caveat

Worth zooming out for a moment. Everything in this section is about borrowing - accepting an LTV ratio, watching a health factor, accepting that a sharp BTC drawdown can force the position to unwind. That's one way to use capital in crypto. It isn't the only way. There's a separate product category - Bitcoin accumulation through a credit structure - that doesn't involve pledging existing BTC as collateral at all. Worth covering separately, since the design problem and the design choices are different.

A Different Category: Bitcoin Accumulation Through a Credit Structure

Worth flagging up front: this isn't another type of crypto loan to compare with CeFi vs DeFi lending. It's a different product category entirely. With a classical BTC-backed loan, you start with BTC you already own and borrow against it. With a Bitcoin accumulation credit structure, you start with stablecoin capital you'd like to grow into a BTC position - and the platform contributes matched credit so the combined sum buys more BTC than your stablecoin deposit alone could. You're not borrowing against existing assets. You're building a new Bitcoin position with capital that's partly yours and partly extended on credit. The two products solve different problems for different users - and a few platforms beyond Binaxity now offer variations of this accumulation-through-credit model, with differences in custody arrangements, interest schedules, and minimum entry.

Binaxity's Bitcoin Investment Line of Credit is the working example we'll walk through. The mechanics:

You deposit stablecoins - USDC or USDT - into the platform. Minimum is $50. You don't need to own any BTC to start, which matters more than it sounds. (Standard KYC checks still apply, like any regulated platform - onboarding can be declined for sanctioned jurisdictions or non-compliant documentation.)

Binaxity adds matched credit from its own capital - 1:1 against your stablecoin deposit. The combined sum is what acquires BTC for your position.

The BTC is purchased and held with qualified custodians via Fireblocks MPC infrastructure inside a bankruptcy-remote SPV. Client assets sit inside an institutional custody arrangement rather than on the operator's general balance sheet.

You service interest only on the credit portion - Binaxity's matched half. Simple, non-compounding, paid monthly. That's genuinely different from most CeFi crypto lenders, which compound interest on the way through. Nexo, for one, is openly compound. The principal isn't amortized during the 12-month term - it stays at the original matched amount, with refinance offered before the term ends.

Where this design diverges most from a classical collateralized loan is around price drawdowns. In a normal BTC-backed loan, a 30–40% drop in BTC price hits a margin call (CeFi) or atomic on-chain liquidation (DeFi), and the loan gets unwound at the worst price. Because the accumulation credit structure isn't a collateralized loan against existing BTC, there's no LTV ratio attached to the BTC price and no margin-call mechanism in the design. That specific failure mode isn't part of the picture. A position can still close without the client's initiative in three narrow cases: a payment more than 90 days overdue, a regulator or law-enforcement order, or a BTC price drop exceeding 90% versus the opening position price. Outside those edge cases, routine drawdowns don't force an exit. Other risks remain - platform counterparty risk, custody risk if the qualified custodian is compromised, operational risk, regulatory risk. The trade-off is real, just shaped differently from a loan-against-collateral product.

How the Accumulation Credit Structure Compares Against CeFi/DeFi Risks

Useful framing here: these aren't head-to-head loan comparisons. A classical BTC-backed loan and a Bitcoin accumulation credit structure address different user goals. Still, the comparison helps clarify which risks travel with which design choice - particularly for someone choosing how to deploy capital across the broader CeFi/DeFi landscape.

Risk discussed earlier | How a classical loan handles it | How the accumulation credit structure handles it |

Rehypothecated custody (Celsius pattern) | User's pledged BTC sits in the platform's omnibus wallet, available for redeployment | Client BTC held by qualified custodian inside a bankruptcy-remote SPV under an institutional custody arrangement |

Platform insolvency (FTX, Genesis pattern) | User becomes unsecured creditor in Chapter 11 | SPV structure is intended to keep client BTC distinct from the operator's general estate (legal outcomes still depend on jurisdiction) |

Forced liquidation on drawdown | Margin call or atomic on-chain liquidation at LTV breach | No LTV threshold attaches; routine price drops don't force an exit. Closure outside the client's control is limited to narrow cases - prolonged non-payment, a regulatory order, or a 90%+ BTC collapse vs. opening. |

Smart contract / bridge exploit (DeFi) | Single protocol exploit can wipe deposits in one block | No direct exposure to DeFi protocol surface; BTC held in qualified custody |

Compound interest accumulation | Standard practice across most CeFi lenders (Nexo confirms) | Simple, non-compounding interest on the credit portion only |

Two Different Things to Do With Your Capital

A practical way to read this table: not as "two competing loans," but as two different actions a user might take with their capital. One is borrowing against existing BTC. The other is building a BTC position with combined capital. Different starting points, different mechanics, different risks.

Parameter | Action: take a BTC-backed loan (CeFi or DeFi) | Action: build a BTC position via accumulation credit (Binaxity model) |

Existing BTC required to start | Yes - user must pledge BTC as collateral | No - user contributes stablecoin capital |

Trigger for forced liquidation | Margin call (CeFi) or LTV breach (DeFi) | Not applicable as an LTV trigger; closure outside the client's control limited to 90+ days overdue, regulatory order, or 90%+ BTC drop vs. opening |

Custody during the term | Platform's omnibus wallet or DeFi smart contract | Qualified custodian inside a bankruptcy-remote SPV |

Principal repayment during term | Scheduled, defined by loan terms | Monthly interest-only on the credit portion; principal not amortized during the 12-month term, with refinance offered before term end |

Outcome on a 40% BTC drawdown | Liquidation crystallises loss at the bottom | No mandatory exit; position remains open, though the floating rate may rise during deep drawdowns |

Minimum entry | Requires existing BTC holdings worth the desired collateral amount | $50 stablecoin deposit, no BTC required |

The honest read is that you're picking the action that matches your goal. If your goal is liquidity against BTC you already own, that's a loan - accept the LTV mechanics that come with it. If your goal is to build a larger BTC position than your stablecoin capital alone could buy, that's an accumulation product - accept the ongoing interest on the credit portion in exchange for combined-capital purchasing power. The risks are real on both sides (counterparty, custody, regulatory), just shaped by the design choices of each product. For long-horizon Bitcoin accumulators starting from cash rather than an existing BTC stack - which is most first-time buyers and a non-trivial slice of long-term builders - the accumulation route is the relevant one.

Security and Failure Modes

CeFi and DeFi don't just have "more" or "less" security. They fail in genuinely different shapes. CeFi failures are concentrated and dramatic: a platform goes bankrupt, a hot wallet gets drained, a regulator orders a freeze and everyone's locked out at once. DeFi failures are scattered and frequent: this protocol gets exploited today, that oracle gets manipulated next month, some bridge breaks somewhere over the weekend. Holding positions across both worlds isn't just diversifying counterparties - it's diversifying across failure categories, which is a subtly different thing.

Failure Type | Where It Occurs | Recent Example | User Recovery Options |

Platform insolvency | CeFi | Celsius / FTX / Genesis, 2022–2023 | Chapter 11 unsecured creditor claim, partial multi-year recovery |

Hot-wallet hack | CeFi | Bybit, $1.4B, Feb 21, 2025 (Safe{Wallet} UI compromise, Lazarus Group) | Platform reimbursement if reserves cover the loss |

Smart contract / bridge exploit | DeFi | KelpDAO, $292M, April 18, 2026 (1-of-1 verifier) | Voluntary protocol restitution; rare and partial |

Oracle manipulation | DeFi | Mango Markets, ~$117M, October 2022 | Negotiated returns; criminal prosecution in some cases |

Cross-chain bridge exploit | DeFi | Ronin, $625M, 2022; Wormhole, $320M, 2022; KelpDAO/LayerZero, 2026 | Treasury-funded reimbursement (rare); usually unrecoverable |

Regulatory enforcement | CeFi | Binance DOJ, $4.3B settlement, 2023; BitMEX, 2020 | None for users directly; geographic restrictions follow |

Chainalysis puts 2025's total at $3.4 billion stolen across the crypto ecosystem. That's a big number on its own. What's striking is the breakdown: centralized service compromises accounted for 88% of Q1 2025 losses, almost entirely because of one event - Bybit. DeFi, despite holding far more TVL than before, kept its hack losses suppressed through 2024 and most of 2025. Protocol-level security genuinely got better. Then April 2026 happened, and the picture flipped again: Drift Protocol drained for $285M on April 1, KelpDAO for $292M on April 18. The pattern doesn't stay still for long.

Regulatory Landscape - Where Each Stands in 2026

The story used to be simple: "CeFi is regulated, DeFi isn't." That hasn't been accurate for a while. Today, CeFi has hard rules in a growing list of jurisdictions - MiCA fully in force in the EU since December 30, 2024, the GENIUS Act signed into US law on July 18, 2025, the MAS regime in Singapore, VARA in the UAE. DeFi is still in a legal grey zone on paper. But regulators have closed the practical gap more than the textbooks suggest. The FATF Travel Rule keeps expanding to VASPs across more jurisdictions, and US agencies have been quietly framing front-end operators as de facto intermediaries - even when the smart contracts behind them are autonomous.

On the CeFi side, MiCA introduced CASP licensing across all 27 EU member states. Capital requirements run €50k–€150k depending on the service. Client-asset segregation is mandatory. The transitional period for existing CASPs runs out on July 1, 2026 - that's the deadline per ESMA's April 17, 2026 statement, and any unauthorised platform serving EU clients after that date is in breach of EU law. Full stop. In the US, the GENIUS Act became the first federal framework for payment stablecoins, requiring 100% reserve backing in liquid assets and monthly public disclosures. The broader market-structure CLARITY Act (H.R. 3633) is the one to watch - it cleared the Senate Banking Committee 15-9 on May 14, 2026 and now needs 60 votes on the Senate floor to become law. FIT21, its 2024 House predecessor, never made it on its own - its provisions ended up folded into CLARITY.

The DeFi picture is messier and more interesting. Protocols themselves technically fall outside CASP licensing when no identifiable operator exists. But front-ends - the websites people actually use to interact with those protocols - do face regulator action. The most-cited 2024–2025 precedent: the SEC issued a Wells Notice to Uniswap Labs in April 2024, then quietly closed the investigation without enforcement action on February 25, 2025. Reading between the lines, a smart contract by itself isn't an "exchange" in the SEC's interpretation. Meanwhile, the FATF Travel Rule's expansion is pushing some jurisdictions to demand KYC from DeFi front-ends operating locally. So the contract layer stays globally accessible. The front-end layer keeps getting geofenced. Which one you sit closer to determines what laws apply to you.

Similarities Between DeFi and CeFi

It's easy to read about the differences and conclude defi and cefi are opposing universes. They aren't. They share more infrastructure than people realize - public blockchains as the settlement layer, stablecoins as the working unit of account, the same financial primitives underneath (spot exchange, credit, margin, derivatives). At the UX level, the lines have actually blurred so far that most retail users can't tell which side they're on. Open Coinbase Wallet, or Binance Web3 Wallet, and you're using DeFi inside a CeFi-branded interface. There's even a name for the overlap zone - CeDeFi - describing platforms that pair licensed custody with on-chain execution.

What both worlds genuinely share:

Public blockchain rails for settlement (Ethereum, Solana, Bitcoin)

USD-pegged stablecoins as primary unit of account (USDT, USDC, DAI/USDS)

Identical exposure to crypto market volatility and macro liquidity flows

Rising interoperability via wrapped assets (wBTC, tBTC) and cross-chain bridges

Cross-border value transfer faster and cheaper than legacy SWIFT/ACH rails

Tax obligations apply in most jurisdictions (the IRS treats crypto as property under Notice 2014-21, regardless of whether earned via CeFi or DeFi)

Which One Should You Choose? A Practical Decision Framework

The choice doesn't come down to ideology. It comes down to two questions you should be able to answer honestly. First: which kind of risk are you actually OK with - counterparty in CeFi, technical in DeFi? Second: how much self-management can you realistically sustain over time? Seed phrase custody, MEV protection, gas optimization, position monitoring at 3am when something starts misbehaving. If the honest answer to the second question is "not much," that's information.

Your Situation | Better Fit | Why |

First-time crypto buyer needing fiat on-ramp | CeFi | Native KYC, card and bank rails, account recovery |

Long-term BTC accumulator wanting regulated structure | Qualified-custody platforms (custody or accumulation products) | Bankruptcy-remote SPV custody arrangements with institutional custodians |

Active trader seeking deep liquidity | CeFi (for now) | Order books still carry tighter spreads on large pairs |

Yield farmer chasing variable APYs | DeFi | Real-time utilization-based rates, composable strategies |

User in restricted jurisdiction blocked from major CEXes | DeFi | Permissionless contract layer; mind geofenced front-ends |

Privacy-conscious user avoiding KYC | DeFi | No identity required at the protocol layer |

User wanting exposure without managing keys | CeFi | Custodial UX, account-style recovery |

Sophisticated user comfortable with smart contracts | DeFi | Full transparency, composability, no withdrawal gates |

Passive earner (staking ETH or stablecoin yield) | Either, with trade-offs | CeFi staking is simple but custodial; DeFi liquid staking via Lido or Rocket Pool keeps custody but adds smart-contract risk |

Most active crypto users, in my experience, don't actually pick one. They use both, for different jobs. CeFi for fiat on/off-ramps and long-term custody at a qualified custodian where the cost of mistakes is high. DeFi for active strategies, jurisdiction-blocked access, and exposure to protocols that simply don't have a CeFi equivalent. The framing that survives contact with reality is treating them as two different toolkits - each one engineered to survive a different class of event.

If your aim is to build a long-term Bitcoin position with combined capital - your stablecoin contribution plus matched credit - rather than borrow against existing BTC, Binaxity's Bitcoin Investment Line of Credit is one structured way to do that, sitting in a different category from the CeFi and DeFi loan products covered above.

FAQ

What is CeFi?

CeFi (centralized finance) is the model where a real, identifiable company - Coinbase, Binance, Kraken - holds your crypto, runs the order book, and processes KYC. You get convenience and human customer support. In exchange, you take on counterparty risk. If the platform fails, your balance becomes a creditor claim, which usually means waiting years for partial recovery.

What is DeFi and CeFi?

Asked another way, the question of what is cefi and defi boils down to two completely different approaches to crypto financial services. DeFi protocols run as smart contracts where you keep custody yourself. CeFi platforms hold user assets as a regulated intermediary. They coexist through wrapped BTC, CeDeFi gateways, and exchange-issued stablecoins that move value between the two worlds every day.

CeFi vs DeFi What is the Difference?

The core difference in cefi vs defi comes back to custody. A CeFi platform holds your keys and your assets. A DeFi protocol holds neither - your wallet does. Every other difference (KYC, fees, transparency, failure mode) is really just downstream of that one structural fork. That's what is cefi vs defi reduced to the part that actually matters.

Is DeFi safer than CeFi?

Neither is universally safer. They just fail differently. CeFi failures are rare but catastrophic - Celsius and FTX wiped out user balances at the platform level. DeFi failures are more frequent but contained - KelpDAO's $292M April 2026 exploit didn't drain other protocols holding rsETH that weren't touched.

Can I use both CeFi and DeFi at the same time?

Yes, and honestly most active crypto users do. The common pattern: buy on a regulated CeFi exchange with fiat, withdraw to a non-custodial wallet, deploy into DeFi protocols for yield or strategy, then route back through CeFi when you need to off-ramp.

Why does CeFi require KYC and DeFi doesn't?

CeFi platforms are regulated intermediaries, which means they're subject to AML, KYC, and FATF Travel Rule obligations in whatever jurisdiction licenses them. DeFi protocols at the contract layer don't have an identifiable operator who can be made to enforce those rules. Front-ends and fiat gateways are a different story - they still impose KYC wherever local law requires.

What happened to CeFi lenders like Celsius and BlockFi?

A Chapter 11 cascade between mid-2022 and early 2023 took down Celsius, Voyager, BlockFi, FTX, and Genesis. The driver was rehypothecation losses combined with Three Arrows Capital, FTX, and Alameda exposure during the market downturn. User balances became unsecured creditor claims, with partial recoveries playing out slowly over multiple years.

Is DeFi legal?

DeFi isn't illegal in most jurisdictions. But the regulatory status of specific protocols and front-ends keeps evolving. MiCA, expanding US enforcement, and the FATF Travel Rule are the three forces actually shaping things on the ground. The net result is a widening gap between globally accessible smart contracts and geofenced front-end interfaces.

Does DeFi work for Bitcoin?

Yes, but indirectly. Most BTC in DeFi sits as wrapped versions (wBTC, tBTC) on Ethereum and other chains. Native BTC-DeFi protocols - Babylon, Merlin, Stacks - are growing fast, but they still represent a small share of total DeFi TVL.